Why audit firms aren’t underpricing their work—they’re overpaying to execute it.

A $100K audit engagement should be a strong piece of business.

It’s large enough to matter, complex enough to justify senior oversight, and priced at a level that should leave room for healthy margin. And yet, for many firms, $100K audits feel harder than they should—staffing pressure mounts, review cycles stretch, and margins fluctuate more than leaders would like to admit.

For years, the conversation around audit economics has focused on pricing. Rates are too low. Clients push back. Competition is fierce.

But after dozens of conversations with audit leaders, managers, and engagement teams, a different picture emerged. Again and again, firms tell us that it’s not that the audit is underpriced. It’s that it costs too much to deliver.

This analysis draws on operational benchmarks from the 2025 IPA Practice Management Report alongside conversations with audit partners, managers, and engagement teams across dozens of firms. By listening to where teams consistently got stuck—and then modeling the cost of those inefficiencies—we uncovered the true economics hiding inside a $100K audit.

The $100K Audit Illusion

On paper, a $100K audit looks profitable.

Firms raise rates to keep pace with inflation. Scopes are negotiated carefully. Engagement budgets are set with experience and discipline. Yet despite all of this, margins remain stubbornly constrained.

Industry data supports what firms are feeling: personnel costs now average 49% of net revenue, and even high-growth firms that outperform the market do so not by charging dramatically more, but by operating differently. Their personnel costs are closer to 43.5%, a gap that compounds meaningfully at scale.

The implication is important.

If pricing were the real issue, margin improvement would track with rate increases. Instead, it tracks with how audits are executed.

Pricing debates, while necessary, often distract from the harder question: Why does it cost so much to deliver the audit in the first place?

Where the Money Actually Goes

To understand audit economics, you have to start with the work itself.

In our customer conversations, one theme came up repeatedly: large portions of the audit are consumed by work that feels necessary, but not particularly valuable. When we mapped those workflows across firms, the patterns were strikingly consistent.

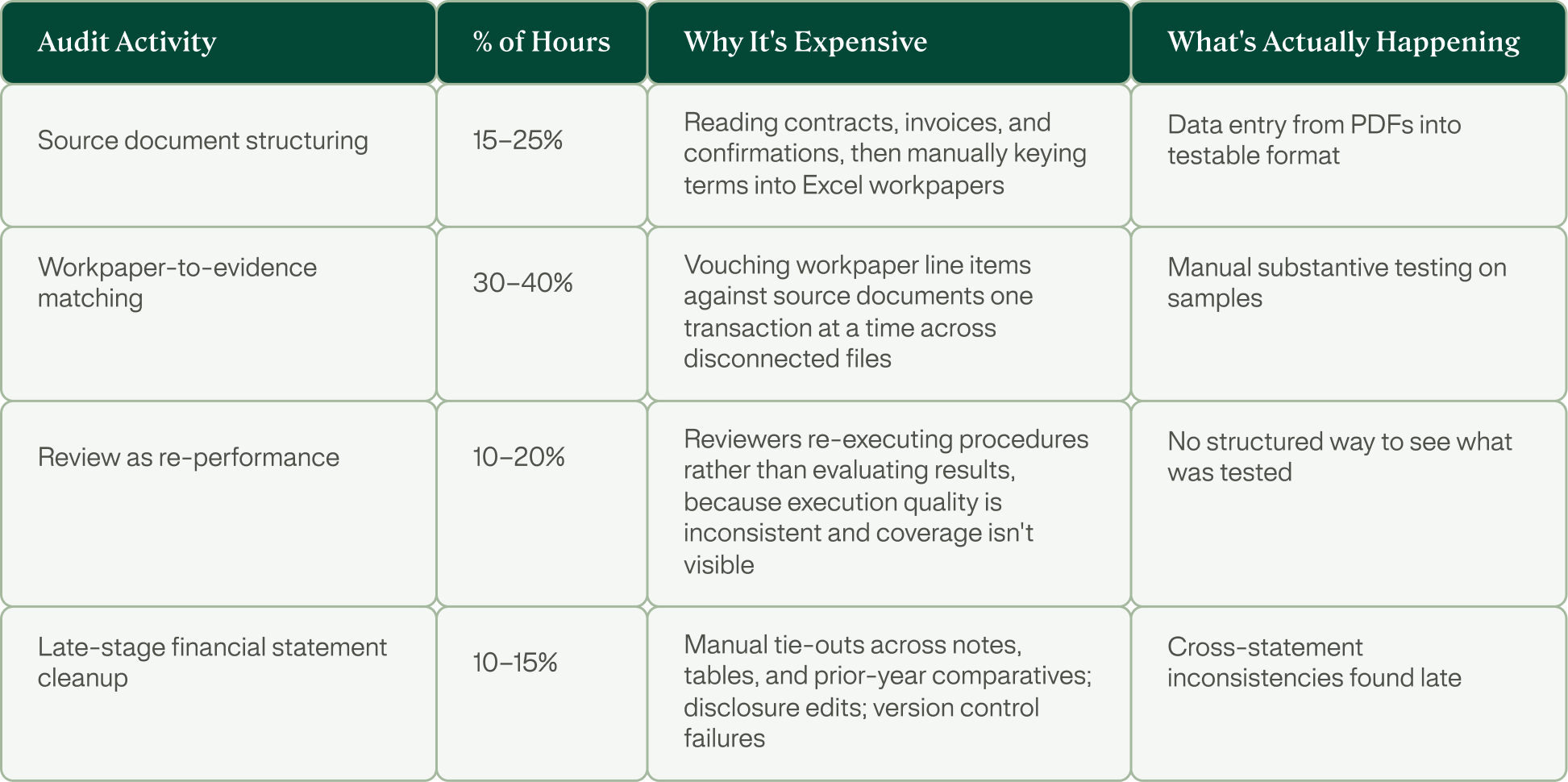

Across engagements, audit hours are largely concentrated in four areas:

Together, these activities consume 65–90% of audit hours, yet they contribute minimal incremental professional judgment.

This is the hidden cost of the modern audit. Firms aren’t paying for judgment alone; they’re paying for the friction created by manual, disconnected execution.

The Talent Tax: How Current Workflows Break Capacity

The cost of inefficient execution doesn’t stop at hours—it spills directly into staffing and capacity.

Firms today average 11.8 FTEs per equity partner, a number that has barely moved year over year. As audit volume increases, capacity doesn’t scale cleanly. Instead, seniors and partners are pulled deeper into execution to keep engagements on track.

The result:

- Partners logging 1,100+ charge hours

- Seniors stretched between review and rework

- A workforce where 52% of professionals are now non-CPAs, increasing review effort when execution is inconsistent

Capacity doesn’t break because demand grows. It breaks because execution doesn’t scale.

When workflows are manual and variable, every new engagement increases the burden on experienced talent. Review becomes re-performance, and judgment time gets crowded out by correction.

The Actual Cost of a $100K Audit

This is where the economics become tangible.

Let’s start with the basics.

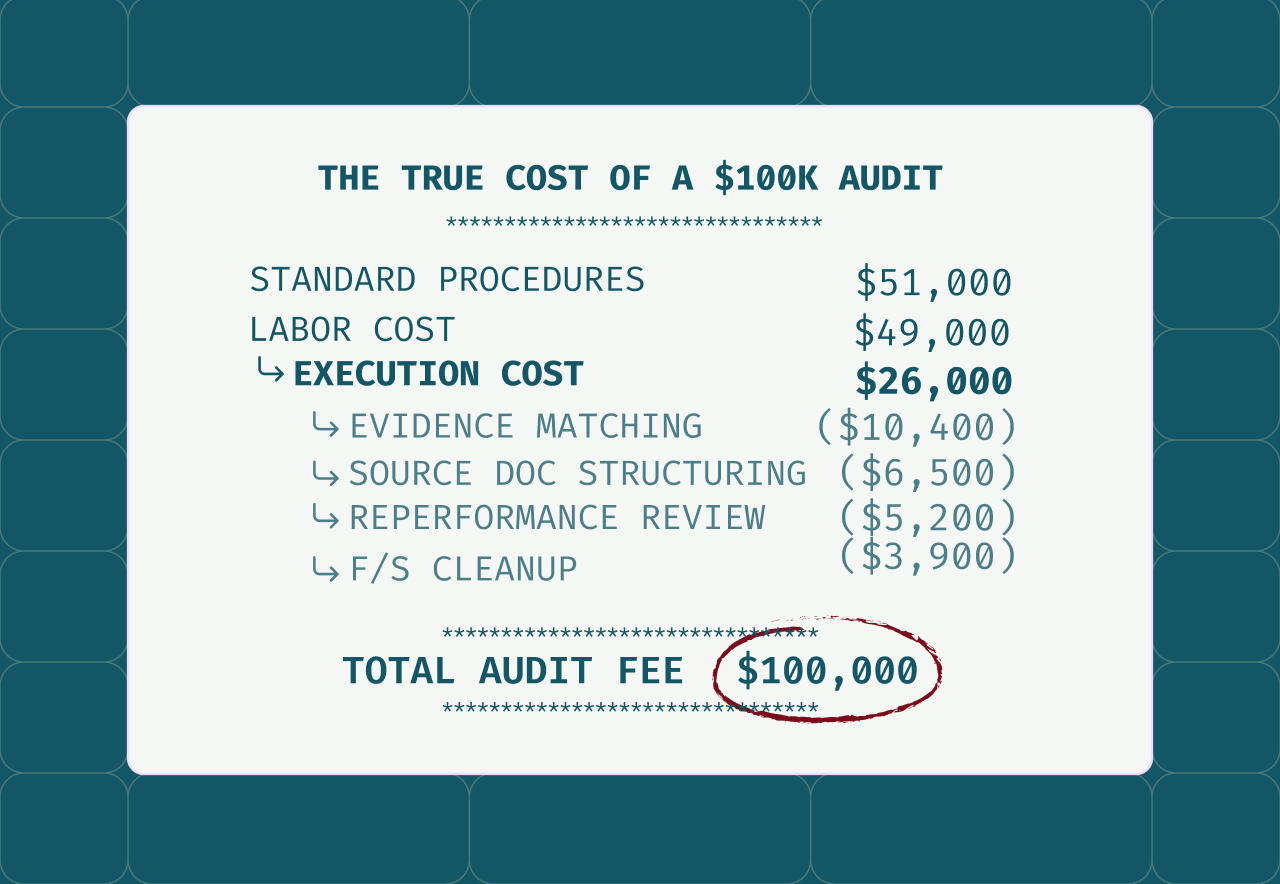

Audit fee: $100,000

With personnel costs averaging 49% of revenue, that means approximately:

$49,000 in labor cost tied to delivering the engagement.

Not all of that labor cost goes to the same kind of work. Based on how audit engagements are typically structured, roughly half of those personnel hours are consumed by the four execution-heavy activities identified above—source document structuring, workpaper-to-evidence matching, review re-performance, and financial statement cleanup. That translates to approximately $26,000 of revenue.

When we map that cost back to the work itself, the picture becomes even clearer:

- Workpaper-to-evidence matching (30–40%): ~$7.8K–$10.4K

- Source document structuring (15–25%): ~$3.9K–$6.5K

- Review as re-performance (10–20%): ~$2.6K–$5.2K

- Late-stage financial statement cleanup (10–15%): ~$2.6K–$3.9K

Most of this spend is not about applying judgment or evaluating risk. It’s about moving data, checking math, reconciling inconsistencies, and fixing issues late in the process.

This is the true cost of the $100K audit—and it’s largely invisible unless you look for it.

Why Hiring Doesn’t Fix the Problem

When firms feel margin pressure, the instinctive response is to hire.

But hiring adds cost before it adds capacity. New staff inherit the same workflows, the same spreadsheets, and the same variability. Revenue per FTE has lagged inflation for years, not because people aren’t working hard, but because output doesn’t scale with headcount under the current model.

Experience improves judgment.

It does not fix broken execution.

Until execution itself becomes more consistent, adding people simply increases the surface area of the problem.

What Changes When Execution Becomes Controlled

In our conversations with customers, the turning point wasn’t “using AI” or “automating everything.” It was treating execution as a system and ensuring that any AI embedded in that system is auditable, inspectable, and governed rather than opaque

When execution is structured and connected:

- Workflows become repeatable instead of reinvented

- Every step is inspectable vs. trying to navigate black boxes

- Review shifts from re-performance to exception handling

- Judgment is applied where it actually matters

This is the core idea behind a Connected Audit: execution, data, and review are no longer fragmented across tools and spreadsheets. They’re part of a single, connected platform designed to reduce friction and variability.

Automation, in this context, isn’t about speed for its own sake. It’s about discipline and about applying auditable AI that produces deterministic, reviewable results rather than probabilistic suggestions

Rewriting the Economics: The Impact of a Connected Audit

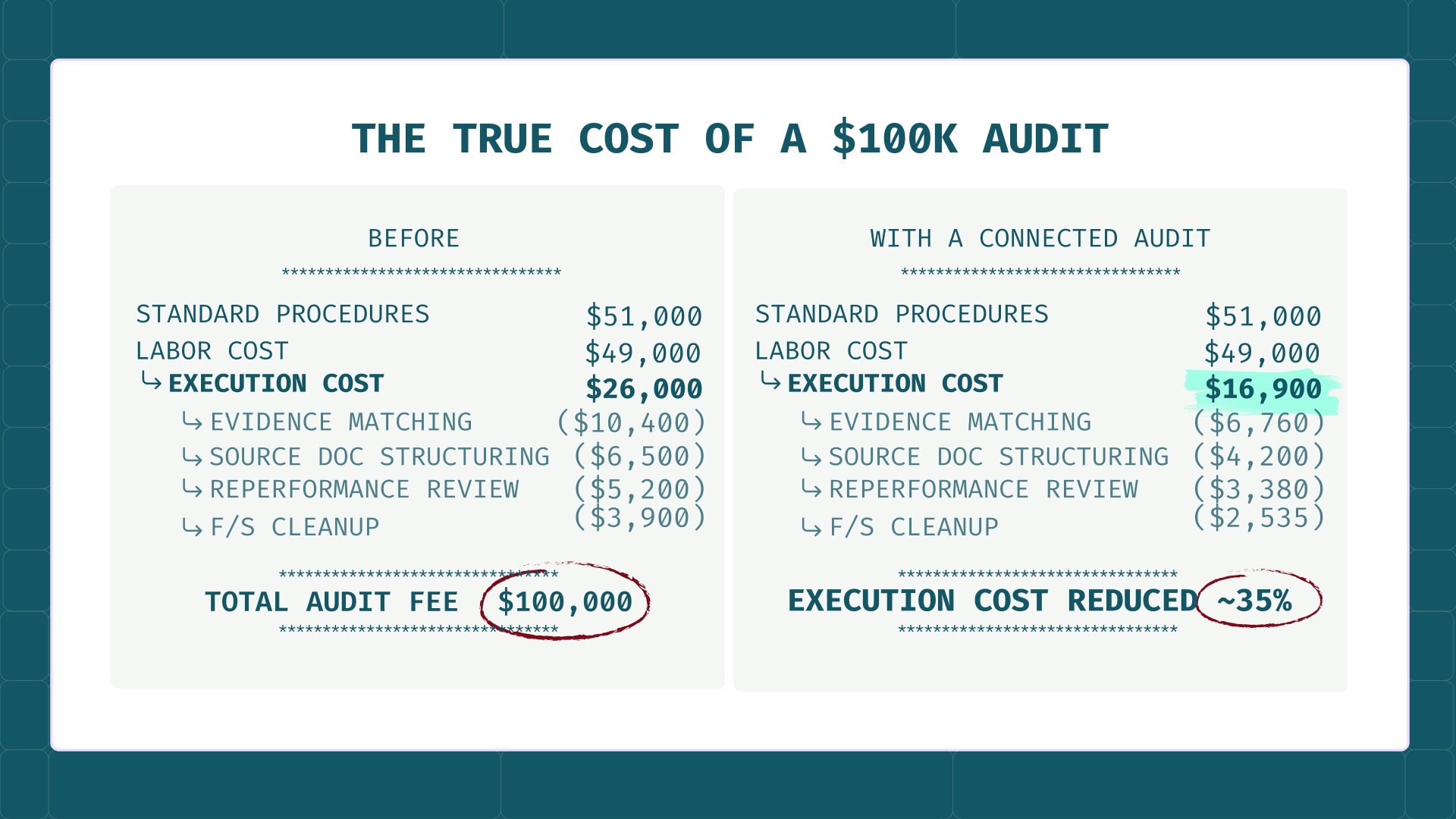

When execution becomes connected and controlled, the economics of the same $1M audit change dramatically.

Across firms using a connected audit approach, we consistently see:

- 40–60% reductions in manual execution hours

- 2–4 FTEs of equivalent capacity unlocked across a portfolio of ~200 engagements

- Review becoming genuinely exception-based

The math is straightforward.

If personnel costs are 49% of revenue, and execution represents roughly 26% of that revenue, reducing execution hours by just 30% creates approximately 3.8 points of margin expansion before accounting for capacity gains.

Revisiting our $100K audit:

- $26K in execution cost

- 30–40% reduction

- $7.8K–$10.4K reclaimed

Same standards. Same audit quality. Radically different economics.

The Choice Firms Face

Audit firms today face a clear choice.

Path one relies on pricing pressure, heroic effort, and headcount growth to protect margin. It works, until it doesn’t.

Path two focuses on standardizing execution, changing the cost per audit, and expanding capacity without hiring.

The true cost of a $100K audit isn’t the fee. It’s the inefficiency firms have learned to tolerate.

And once that cost becomes visible, it becomes optional.

Redesigning the Cost Drivers of the Audit

If the hidden cost of the $100K audit lives inside execution, then improving economics isn’t about working harder, it’s about redesigning how that execution happens.

The four areas consuming the majority of audit hours don’t require less rigor. They require more control. When execution becomes structured, connected, and powered by auditable AI, those same activities shift from manual, variable workflows to deterministic, inspectable systems.

Here’s what that looks like in practice:

1. Source Document Structuring

Suggested change:

Documents are structured into testable workpapers automatically, eliminating manual reading and data entry from PDFs with auditable AI that extracts and structures data in a way that remains traceable to the original source document. The structured output becomes the auditor’s workpaper directly.

What this unlocks:

Auditors stop extracting and reformatting data and instead focus on evaluating the substance of agreements and transactions. Time investment shifts from transcription to judgment.

2. Workpaper-to-Evidence Matching

Suggested change:

Matching logic is generated directly from the audit procedure written in the workpaper, then executed deterministically against PDF evidence across the full population. Results embed back into the original workpaper format with coverage metrics and exception documentation.

What this unlocks:

Substantive testing moves from manual, sample-based vouching to consistent, full-population execution. Coverage becomes visible and measurable, reducing variability and increasing confidence in what was actually tested.

3. Review as Re-Performance

Suggested change:

Reviewers can inspect the test’s underlying logic that was automatically built and see structured coverage metrics—showing exactly what was tested and what wasn’t.

What this unlocks:

Review shifts from re-doing procedures to evaluating exceptions and applying judgment. Mechanics become transparent, allowing reviewers to focus on risk instead of rework.

4. Late-Stage Financial Statement Cleanup

Suggested change:

Mathematical accuracy validation and cross-statement consistency checks—note-to-note, note-to-table, table-to-table, and prior-year comparatives—run automatically. Tie-out and disclosure errors are caught before partner review rather than during it.

What this unlocks:

Cleanup moves upstream. Late-stage fire drills shrink, partner review pressure decreases, and financial statements reach final stages with fewer preventable inconsistencies.

Conclusion: A Better Foundation for the Same Audit

The analysis of a $100 K audit makes one thing clear: the real constraint on audit economics isn’t just pricing, talent, or standards. It’s the foundation the work runs on.

For decades, accounting and audit have relied on fragmented tools, spreadsheets, and manual handoffs to manage increasingly complex, high-stakes work. That model survived when data volumes were smaller, expectations were lower, and execution could afford to be inconsistent. Today, it no longer scales.

As data grows, standards tighten, and scrutiny increases, firms are being asked to do more—faster, deeper, and with greater confidence—on top of an operating model that was never designed for this level of complexity. The result is exactly what we see inside the $1M audit: execution friction, re-performance, late-stage cleanup, and margin pressure that feels unavoidable.

Trullion was built in response to these realities.

Not to replace professional judgment.

Not to force teams into rigid processes.

But to give the profession a modern foundation.

Trullion is a connected platform designed for how modern accounting and audit actually work. At its core, it unifies Agents, Workflows, and Knowledge into one platform, embedding auditable AI—so data, documentation, and judgment move together instead of breaking apart across tools and spreadsheets.

This connected foundation enables two critical outcomes:

- The Connected Firm, where audit and assurance teams standardize execution, test deeper without adding hours, and shift review from re-performance to exception-based evaluation—changing the cost dynamics of every engagement.

- The Connected OCFO, where finance and accounting teams maintain consistency, control, and audit readiness across leases, internal audit, and core accounting operations.

In both cases, the impact is the same: execution becomes predictable, review becomes focused, and economics improve without lowering standards or burning out teams.

The next generation of accounting isn’t louder or more complex.

It’s calmer. More connected. And built to scale with confidence.

If the analysis in this piece mirrors what you’re seeing inside your own audits, mounting execution effort, stretched talent, and margins under pressure, we’d love to compare notes.

Talk to our team to see how a connected audit platform changes the cost, capacity, and confidence of your engagements.