ASC 842 introduced new requirements when it comes to accounting for operating leases. In this article, we’ll go over the main requirements when it comes to accounting for operating leases under ASC 842. We’ll also look at some tips and best practices to ensure that your ASC 842 compliance is seamless and smooth.

What is an Operating Lease?

An operating lease is when one person (the lessor) gives another person (the lessee) access to an asset. Typically, the lessee is allowed to use the assets for less than their economic life span in exchange for a time period during which they make payments.

Operating Lease Accounting Under ASC 842 vs. ASC 840: What changed?

Under ASC 840, an operating lease is treated as an off-balance sheet transaction. Rent expense associated with the arrangement is recognized in the income statement. There is no balance sheet impact. For operating leases, the ASC 842 requires recognition for an ROU asset and a corresponding lease obligation upon lease commencement.

What is the purpose of the FASB lease accounting changes?

FASB ASC 842 increases transparency by increasing disclosure and visibility into the leasing obligations of both public and private organizations.

Ways the ASC 842 Balance Sheet is Different

When it comes to operating leases under previous standards (notably ASC 840) the accounting treatment was relatively straightforward. Operating leases could be expensed through the income statement on a straight line basis.

ASC 842 was released in order to increase transparency and comparability across organizations. Part of the reasoning behind ASC 842’s release was what was perceived as loose rules around operating leases, which enabled certain loopholes that could potentially be taken advantage of.

ASC 842, therefore, mandated that operating leases should be reflected on the balance sheet (as a right-of-use asset and a lease liability), and tightened some of the disclosure requirements around operating leases.

Another key aspect of ASC 842 is the definition of a lease, which is “A contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration.”

An operating lease, from the perspective of the lessee, is further defined as any lease that is not a finance lease.

How to Calculate the Journal Entries for an Operating Lease under ASC 842

We’ll tackle accounting for operating leases under ASC 842 much like the standard (or “Topic”) released by the FASB does.

This includes the following steps (How to Record Journal Entries):

- Recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position

- Recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term on a generally straight-line basis

- Classify all cash payments within operating activities in the statement of cash flows

- Ensure to account for any modifications

ASC 842 also has novel disclosure requirements, with the stated objective of “enabling users of financial statements to assess the amount, timing, and uncertainty of cash flows arising from leases.”

ASC 842, therefore, requires reporting of operating lease liabilities and lease incentive opportunities in the lease agreement. Operating activity includes both qualitative and quantitative disclosures.

What follows is a high-level overview of accounting for operating leases under ASC 842.

Recognition

Classification: first, the entity must classify each component of the lease at the commencement date. If the criteria for classifying a lease as a finance lease are not met, the lease is classified as an operating lease.

Lease modifications: lease modifications can lead to accounting for the updated lease as a new, separate lease. ASC 842 outlines the test to determine which treatment should be applied (842-10-25-8).

Initial Measurement

Lease term: this is the non-cancellable period of the contract that contains a lease or lease element, plus time over which the option to extend the lease is available and it is seen as likely that this option will be exercised; similarly it includes periods where termination is available but is unlikely to be exercised; and finally, periods where the two prior conditions are controlled by the lessor.

Lease payments: this includes fixed and variable lease payments, and is defined in detail in ASC 842 (842-10-30-5). What rate should be used? The rate implicit in the lease should be used when available, and when unavailable, an entity should use its incremental borrowing rate.

Initial direct costs: costs that would have been incurred no matter whether the lease was finalized or not, are not initial direct costs. This includes general overheads, advertising, and tax and legal advice.

Right-of-use asset: This should be measured at the initial measurement of the lease liability, any lease payments made before commencement (net of lease incentives received), and any initial direct costs incurred by the lessee.

Subsequent Measurement

Lease liability and right-of-use asset: the lease liability is measured at the present value of outstanding lease payments, while the right-of-use asset is measured at this amount adjusted for specific elements listed in ASC 842, such as prepaid or accrued lease payments.

Remeasurement: remeasurement, whether of the lease term or lease payments, occurs when a lease modification as defined has taken place.

Disclosure

Balance sheet: separate operating lease assets and liabilities (classified as current and noncurrent, like all assets and liabilities), or which line items in the balance sheet include the right-of-use assets and lease liabilities.

Income statement: lessee’s expenses.

Cash flow statement: payments arising from operating leases.

General disclosure: The following needs to be disclosed from both a qualitative and quantitative perspective. An entity’s:

- Leases

- Significant judgments made in applying ASC 842

- Amounts recognized in the financial statements relating to its leases

Challenges of Accounting for Operating Leases under ASC 842

Of course, what we’ve listed in terms of accounting for operating leases under ASC 842 is a bird’s eye view of the topic. There are many details and exceptions within ASC 842, and we always suggest familiarizing yourself with the standard.

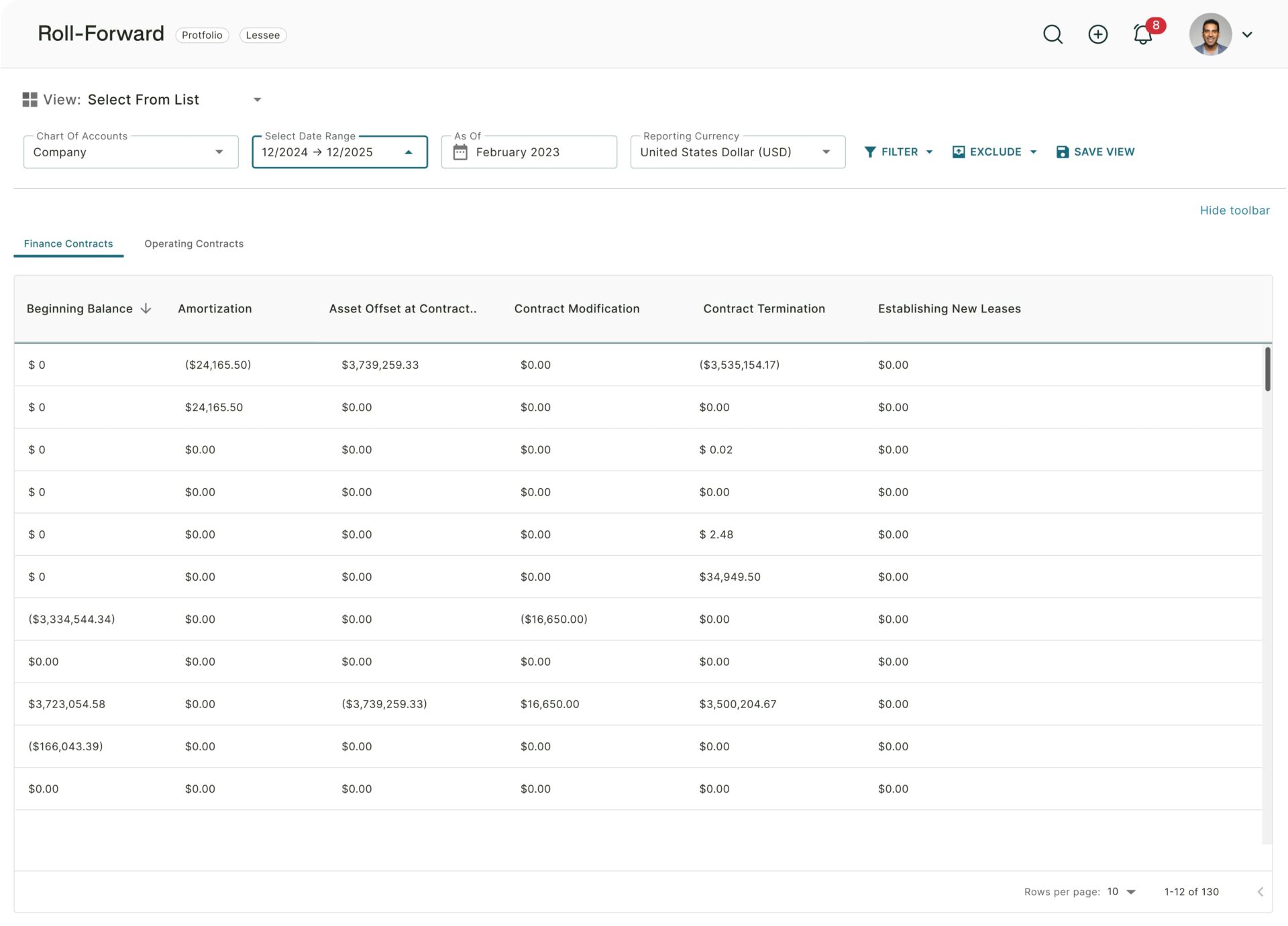

As we’ve seen even from this level of detail, there are significant challenges when it comes to accounting for operating leases under ASC 842. This is why we recommend leaning on technology to come to your aid in order to ensure compliance, prevent errors, mitigate risk and keep your team from getting bogged down in leases all year.

Download the Ultimate Guide to Implementing ASC 842.

Accounting for Operating Leases under ASC 842: With Technology

Trullion is a technology leader that provides an end-to-end lease accounting software solution for taking care of your organization’s leases, using AI-enhanced automation to ensure a level of speed and accuracy that human beings just cannot match.

If you’re interested in finding out how this can boost your business, book a demo.

You’ll be blown away at how a modern solution can transform your business processes and create so much value.